Why Is My Mortgage Company Listed on My Insurance Check? Endorsement issues

Let’s get into it….

When faced with a loss such as a fire, storm, or pipe leak, the last concern on your mind is likely, "Who will be listed on the checks?" Thus, it can be surprising to find that your mortgage company is listed as a payee on your insurance check. This complicates the process for several reasons, most notably because the check cannot be processed without the signatures of all involved parties. Unfortunately, mortgage companies are often slow to provide their endorsement.

"Mortgage companies are often slow to provide their endorsement"

Common Concerns Regarding Second and Third Party Payees

Why does this happen?

What challenges might you face?

How can you resolve these issues?

Why Is the Mortgage Company Listed on the Check?

The primary reason is that it is their right to protect their financial interest in the property. Without their name on the check, funds could be misappropriated, leaving the mortgage company exposed.

When you have a mortgage, your lender holds a vested interest in your property. While some may characterize the mortgage company as a “partial owner” of your home, this is a simplification. The homeowner is listed on the title and deed and is legally considered the owner, while the mortgage company is the owner of the loan.

Understanding this relationship is crucial because homeowners frequently question why their lender appears as a payee on their insurance check. While it is true that you own the home, you also have a legal obligation to the mortgage, which is secured by the property itself. To mitigate the risk of misappropriation of funds, the mortgage company is included as a payee, ensuring that no funds are released without the necessary signatures. Many years ago, there have been people that ran away with the insurance money leaving the mortgage company holding a smoldering pile of rubble.

Common Challenges When the Mortgage Company Is Listed as a Payee

Homeowners often encounter significant delays, extensive documentation requirements, and the need to navigate complex processes.

One of the most pressing issues is the delay in fund release. Mortgage companies frequently refuse to endorse checks exceeding a certain amount (typically $10,000) unless the homeowner provides appropriate documentation. For instance, if a homeowner receives a $35,000 check and has a signed contract with a contractor for repairs of the same amount, the lender may endorse the check based on that contract. Conversely, if there is no signed contract, the mortgage company may place the funds in escrow until the homeowner either completes the repairs or secures a contract.

Mortgage companies often require a variety of documents before releasing funds. These may include signed contracts from contractors, proof of repairs, and specific insurance documentation related to the claim. If the payout is based on an adjuster’s estimate, they may request the “adjuster's worksheet.”

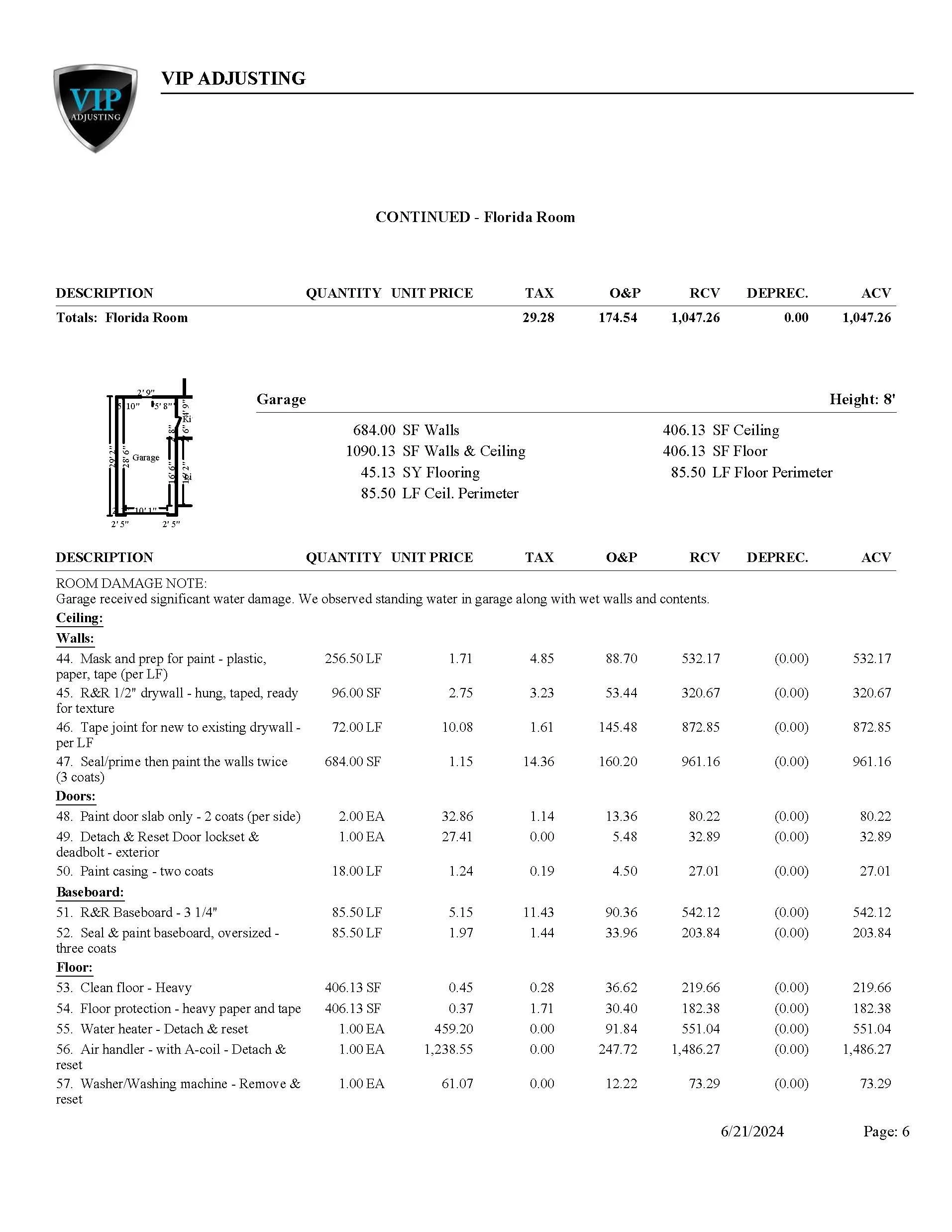

Typical example of a Public Adjuster's Worksheet (aka: estimate)

However, if your claim was settled through negotiation, an “adjuster's worksheet” may not exist to support the agreed amount. In this case, you can submit a signed release document to the lender, which specifies the settlement amount and releases the insurance company from further liability. While this document typically satisfies the need for an “adjuster's worksheet,” it does not guarantee fund release, as the mortgage company must still confirm that repairs will be completed.

How to Obtain a Mortgage Endorsement

Several strategies can facilitate the release of funds from the mortgage company:

Provide signed construction contracts.

Submit material costs along with a letter designating yourself as the contractor.

Engage a Public Adjuster to secure the necessary endorsements.

Submitting a signed contract with a contractor is one effective method to compel a mortgage endorsement. Homeowners should meticulously document all submissions to the mortgage company, ensuring a clear record of communications.

In some states, homeowners may act as their own contractors if the property is their primary residence. In such cases, a well-crafted letter, along with material cost information, can be sent to the mortgage company. However, be prepared for potential confusion, as lenders are accustomed to straightforward processes. If your situation falls outside their standard parameters, it can become an uphill battle.

Furthermore, before the final disbursement of insurance funds, mortgage companies may require an inspection to confirm that repairs have been completed. Scheduling and passing this inspection can introduce additional delays. In certain situations, they may allow you to submit photographs as evidence instead of conducting a physical inspection, but this is not always guaranteed.

The involvement of a Public Adjuster can also prove beneficial, as they often have industry connections that facilitate endorsements for a nominal fee. Our team at VIP Adjusting routinely addresses these challenges and has successfully helped numerous homeowners navigate the endorsement process.

Key Considerations While Managing Your Claim

Communicate Early and Often: As soon as you identify that your mortgage company is listed on the insurance check, contact them for a detailed explanation of their requirements for endorsing and releasing funds. This proactive approach will help you gather the necessary documentation and avoid delays.

Maintain Detailed Records: Keep a comprehensive paper trail of all communications and documents sent to your mortgage company. This can help prevent delays from lost paperwork and provide leverage in case of any disputes.

Be Persistent: Securing the release of funds often requires perseverance. Mortgage companies can be slow to act, and you may need to follow up multiple times to reach someone with the authority to expedite the process.

Seek Assistance if Necessary: If you encounter difficulties in obtaining fund release from the mortgage company, consider reaching out to VIP Adjusting. We can assist in securing a mortgage endorsement and ensure that your claim is thoroughly reviewed. Public adjuster to the rescue!

Conclusion

Navigating the complexities of dealing with a mortgage company listed on an insurance check can be both slow and frustrating. Many clients find this process even more challenging than engaging with their insurance company. However, with effective communication, persistence, and a proactive mindset, you can overcome common obstacles and expedite the release of funds. This allows you to focus on what truly matters: rebuilding your home and your life.

P.S. Some clients have utilized their insurance claim proceeds to pay off their mortgage balance, thereby eliminating the mortgage company from the process. Consult with an adjuster to determine if this is a suitable option for your specific circumstances.

Happy Endorsing!